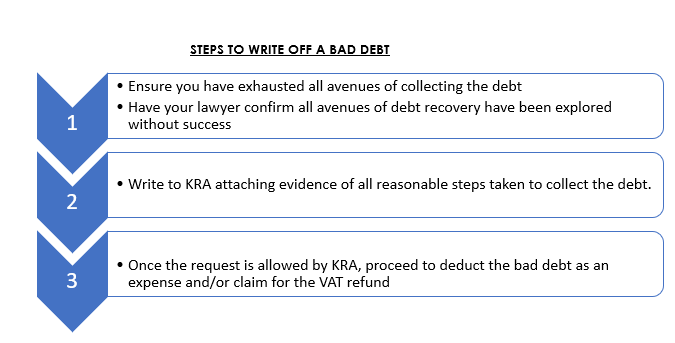

HOW TO LAWFULLY WRITE OFF A BAD DEBT FOR TAX PURPOSES-KRA GUIDELINES

ARE BAD DEBTS ALLOWABLE DEDUCTIONS BY LAW?

In the realm of business operations, encountering non-recoverable debts is an inevitable aspect. However, under Section 15 of the Income Tax Act, there exists a provision that offers relief in such circumstances. This section permits businesses to deduct losses incurred from bad or doubtful debts when computing their taxable income and profits during a financial period.

WHAT QUALIFIES AS A BAD DEBT?

According to the Income Tax Act, a debt is classified as “bad” when it is demonstrated, to the satisfaction of the Commissioner of Domestic Taxes, that despite all reasonable efforts to collect it, the debt remains uncollectable.

HOW DOES A DEBT BECOME UNCOLLECTABLE?

Under the Kenya Revenue Authority Guidelines On Allowability Of Bad Debts (Legal Notice No. 37 of 2011) a debt is deemed to have become uncollectable if any one of these conditions are met/proven:

- The creditor loses the legal right to collect the debt through a court order.

- There’s no way to get back any security or collateral, either in part or in full.

- Even if there were security or collateral, selling it doesn’t cover the whole debt.

- The debtor is declared bankrupt or insolvent by a court, or is under administration.

- The cost of trying to collect the debt is more than the debt itself.

- Efforts to collect the debt are abandoned for another reasonable cause.